I Stand Corrected

I Stand Corrected

w.214 | Seed Investing, Holding Cash, Convoy, Startups shutting down

Dear Friends,

It has been non-stop this fall, and we now have only two months left in 2023. A new reality seems to be settling in. Multiple people this week have referenced Howard Marks’ Sea Change memo to me; usually, despite my interest in the topic, no one outside one text chain ever talks to me about Marks’ memos.

Today's Contents:

Good Reads: Sensible Investing

Song of the Week: I Stand Corrected

Good Reads: Sensible Investing

Seed Investing - Is It a Sea Change?

Seed Investing - WTF is Going on (Links to the deck and doesn’t require email). Where the opportunities are and what to avoid from Sam Lessin.

It’s worth a read, even if it could be a medium-length blog post. Some parts are stronger than others, and more data would make his arguments more compelling.

The strongest part is the ‘where to go theory,’ and that part founders, GPs, and LPs alike should reflect on.

His ‘where to hunt’ (the next page) is more complicated. We’ve looked at those themes (SMBs, creators, etc.) for a long time, and I agree there is opportunity there, but it requires care.

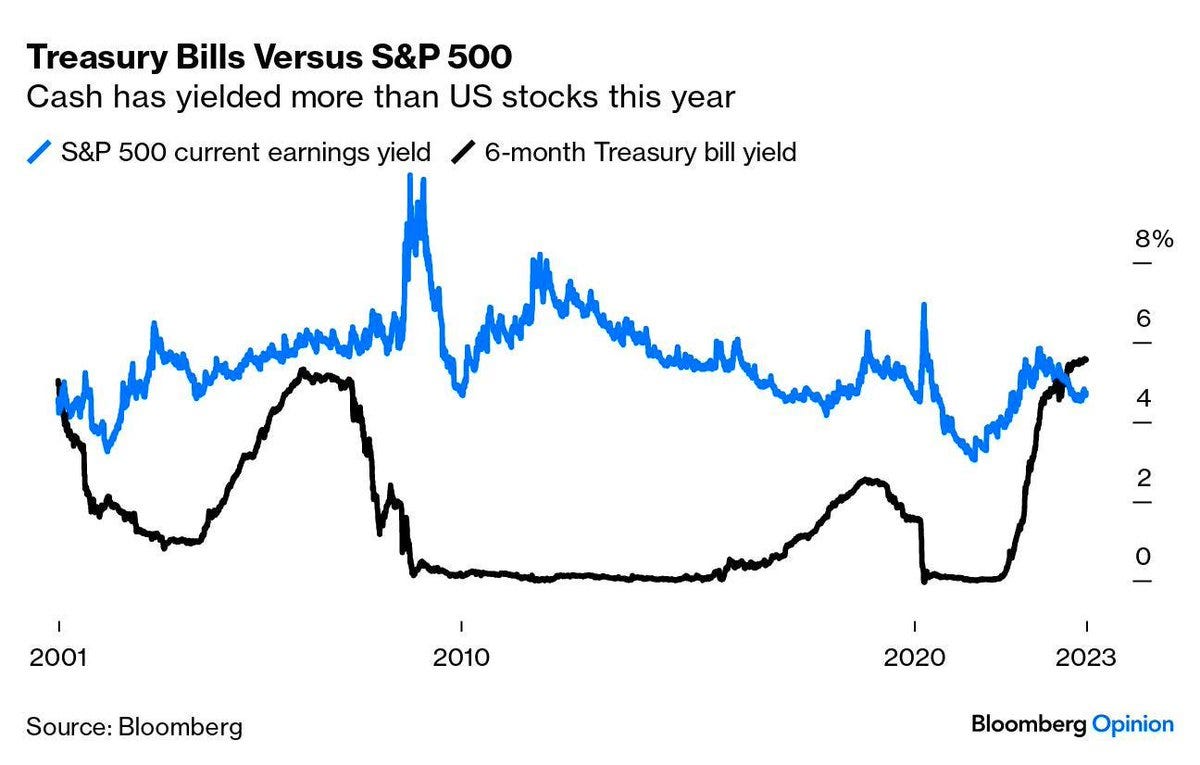

Painful Decision to Hold Cash by Seth Klarman in the Baupost Year End Letter 2004. This two-pager is worth the read and essential to remember when the market is resetting and repricing every category. Of course, he’s referring to public market investing, but there is enough wisdom for alternatives.

Those in the investment business compete on the basis of short-term, relative (not absolute) investment performance, and prefer to follow the herd (at the price of assured mediocrity) rather than stand apart (risking severe underperformance). From a business perspective, how much better to be actively deploying capital, even if the investments are mediocre, than to be stalled in neutral; the employees keep busy, while the clients confuse decisions with diligence, activity with insight, and a fully invested posture with a worthwhile portfolio.

Betting that the markets never revert to historical norms, that we are in a new era of higher securities prices and lower returns, involves the risk of significant capital impairment. Betting that prices will fall at some point involves opportunity cost of uncertain amount. By holding expensive securities with low prospective returns, people choose to risk actual loss. We prefer the risk of lost opportunity to that of lost capital, and agree wholeheartedly with the sentiment espoused by respected value investor Jean-Marie Eveillard, when he said, "I would rather lose half our shareholders... than lose half of our shareholders' money.

The days of ‘Cash is Trash’ are over.

See the graphic below.

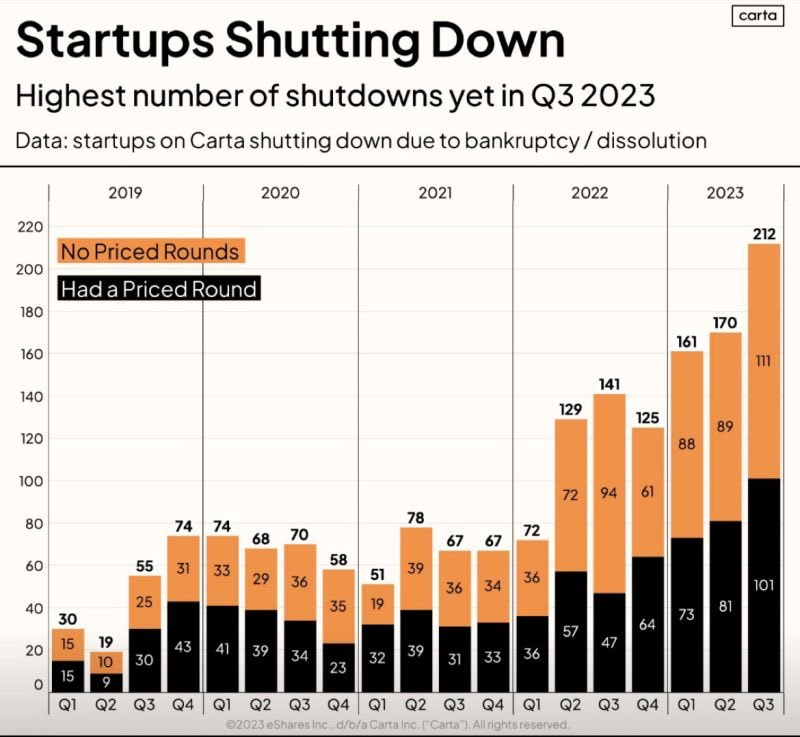

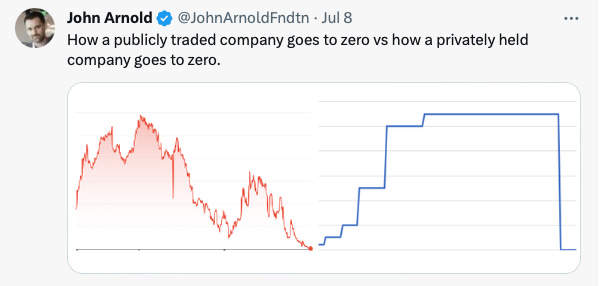

Startups shutting down

The startup shutdowns are beginning to show up in the data. I’d estimate that Carta and AngelList data is at minimum two quarters lagging reality.

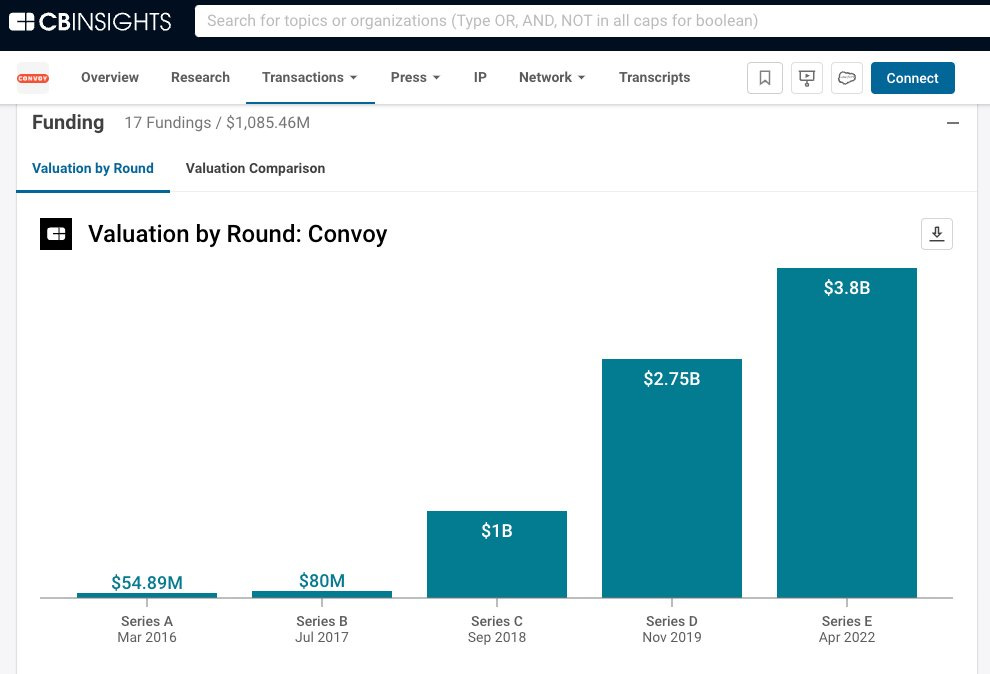

The most recent prominent example of startup shutdowns is Convoy, a logistics company, which announced massive layoffs and winding down its core business last week.

We are still in the early innings of startup failures from blitz-scaling businesses. Many of these will leave massive holes in portfolios as markdowns in private markets are slow to adjust. The charts below show the build-up and then the crash.

Death from Overfunding: An Obituary For Convoy from Zero Hedge.

Commoditizing Logistics: Assessing 'Disruptive’ Links in the Supply Chain

I won’t claim to know about the freight market - but I asked Matt Reustle, the equity analyst from Goldman Sachs, to send me this report in 2018 that explains that maybe tech could expand logistics net margin by 16-18%. He turned out to be right!

But the biggest misconception (to me) was investors viewing Convoy (or whatever "freight disruptor") like a Bloomberg for freight. "Say goodbye to phone calls. Hello software!" But it's not the case. TMS (Transportation Management Software) acts as the Bloomberg. Those were run by....Oracle, SAP, etc. And these "disruptors" had APIs that plugged into them.

Obviously The Future…What’s Next?

Thanks for the thoughts and feedback on all the podcast/YouTube episodes so far. Next week, we release Episode 7, and most people never get that far. Fear not; the next seven in the queue, so we aren’t going away.

The next three episodes are with Austin-based leaders who are experts in curating communities, hosting events, and making new friends.

Song of the Week: I Stand Corrected

Video on YouTube.

I like Vampire Weekend and this song. Their 2008 album is a quick listen, and all the songs have tight, intelligent lyrics.

“I Stand Corrected” by Vampire Weekend

You've been checking on my facts

And I admit, I have been lax

In double-screening what I say

It wasn't funny anyway

I stand corrected

I stand correctedSelfie of the Week

A recent highlight was dinner with my old and dear friends from Duke Econ. On my right is Rob, an emerging (hedge fund) manager of Uluwatu Limited. Uluwater is a Hong Kong-based, long-only investment firm that invests long-term in publicly traded, entrepreneur-led businesses across Asia. On my left is Josh, who just wrapped up his first semester as an Adjunct Professor at Columbia, teaching Climate Change and ESG Investing while leading quantitative investing and geospatial modeling at Blackrock.

We’ve come a long way in the 19 years from Econ 55.

Thanks for reading, friends. Please always be in touch.

As always,

Katelyn